ClearPoint Neuro ($CLPT) - Update

The flywheel accelerates...

Today marks three months since I wrote an introductory Substack post about my favorite investment idea, ClearPoint Neuro CLPT 0.00%↑. My intention of utilizing Substack is a selfish one; to engage in a public medium that holds myself accountable to the diligence process and to the conviction I have in the investments I make. This post (and those that will follow) will serve as a sort of investing journal as I continue to grow as an investor and deepen my understanding of the investments I make. In the spirit of complete transparency, CLPT 0.00%↑ is my largest position today at ~18+% of my portfolio with an average cost basis of $7.14. I first took a small starter position in late 2021, added in small quantities over 2022 and 2023 as I built conviction and understanding in the company, and took a significant full position in 1H of 2024. Since writing about CLPT 0.00%↑ just a quarter ago, the company has announced stellar Q2 results and has rightfully been rewarded by the markets. In the near-to-mid term, I expect the stock to go way up, or down, or sideways (nailed it).

Below, I’ll touch on a few of the key highlights and themes from the Q2 earnings call and 10Q that stood out to me.

BDD - Biologics and drug delivery business segment

FNN - Functional neurosurgery and navigation business segment

Growth

Quarterly revenues were a record (I suspect we’re going to be saying that a lot) of $7.9M, despite what appears to have been a relatively weaker quarter from their strongest current business segment Biologics and drug delivery (BDD). Meanwhile, Functional neurosurgery and navigation (FNN) revenue growth far exceeded my expectations following a series of tough quarters where the unit regressed on the loss of a single large partnership with a BCI partner.

What’s changed? Well, the leading indicator for capital sales and subsequent FNN recurring razorblades ($$$) is hospital customers. And hospital customers are ramping significantly in 2024. 8x partnerships in Q1 followed by an additional 6x here in Q2, for context ClearPoint added 8x partnerships in the entirety of FY23.

Let me say that again…

8x hospital customers added in FY23

vs.

14x hospital customers added in the 1H of FY24;

However, hospital partnerships alone are not enough. What we’re seeing translated through the segment are the benefits of hospital customer base acceleration compounded by management’s focus on moving up the value chain by providing expanded and superior offerings than their incumbent competitors. Navigation systems are now rolling out in the MRI suite and the OR, the best (and it’s not even close) laser on the market is now experiencing uptake across 3 tesla applications. Additionally, they’re on track to unlock the remaining ~50% of the market opportunity in FY25 with FDA approval of their 1.5 tesla offering.

Looking ahead

I’ll be looking for BDD revenue to reaccelerate in a lumpy fashion in the quarters ahead. Seven partners are progressing through accelerated FDA processes – fast-track, priority review, and RMAT designations (good source of info here). A handful of these partnerships could result in large, one-time, 100% gross margin milestone payments in addition to ramping product sales.

On the FNN side of the house, I’m very encouraged by the quick adoption SmartFrame OR and PRISM 3T offerings – both moving to full market release ahead of schedule. Further customer adoption is obviously paramount; however, early indications of hospital uptake are very encouraging.

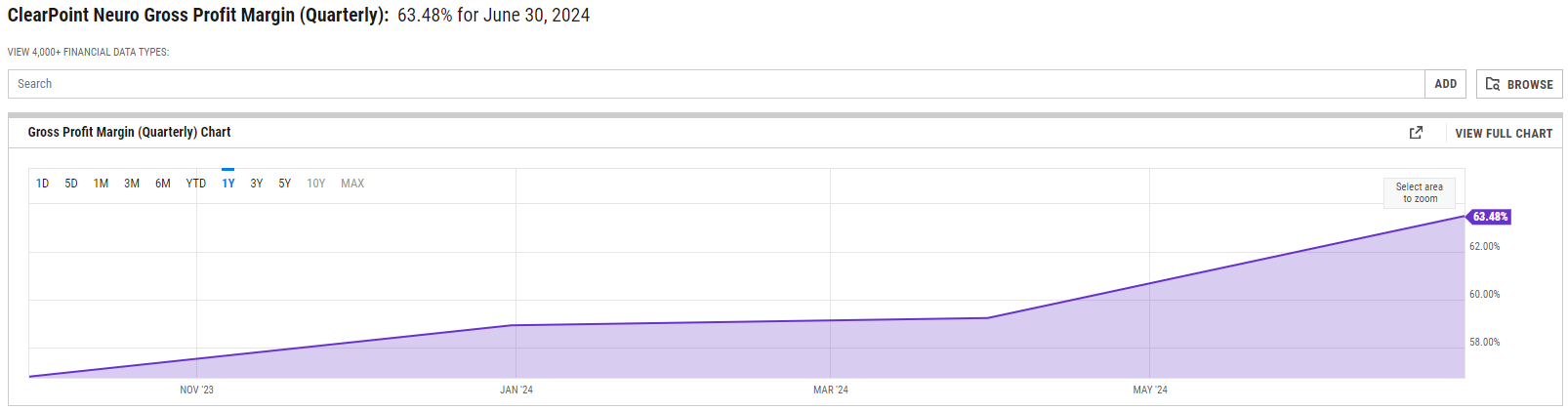

Gross Margin Expansion

The business is currently experiencing significant mix shift from lower margin services into higher margin disposable product sales ($$$) with quarterly product revenue up 112% YoY. I expect this trend to continue on an absolute basis as BDD partners progress through trials and we see increased product sales; and within the FNN segment as we see increasing disposable product revenues from the SmartFrame platform.

Gross margins for the quarter were 63% in Q2, up from 59% sequentially in Q1. Net of one-time impacts from the BDD segment (lumpiness), I expect to see further margin expansion as mix shift continues to move into product sales.

Parting Thoughts

Overall, I continue to come away with a deep level of respect and admiration for what Joe and his team are building at ClearPoint Neuro. Management has shown a keen ability to communicate, continuously refine, and execute upon their long-term strategic initiatives and I am encouraged by what the future holds.

I plan to hold CLPT 0.00%↑ for a long time as the thesis begins to play out.

The flywheel is in motion.

Cheers,

Mike